Back to News

News AlertWorld of Startup’s

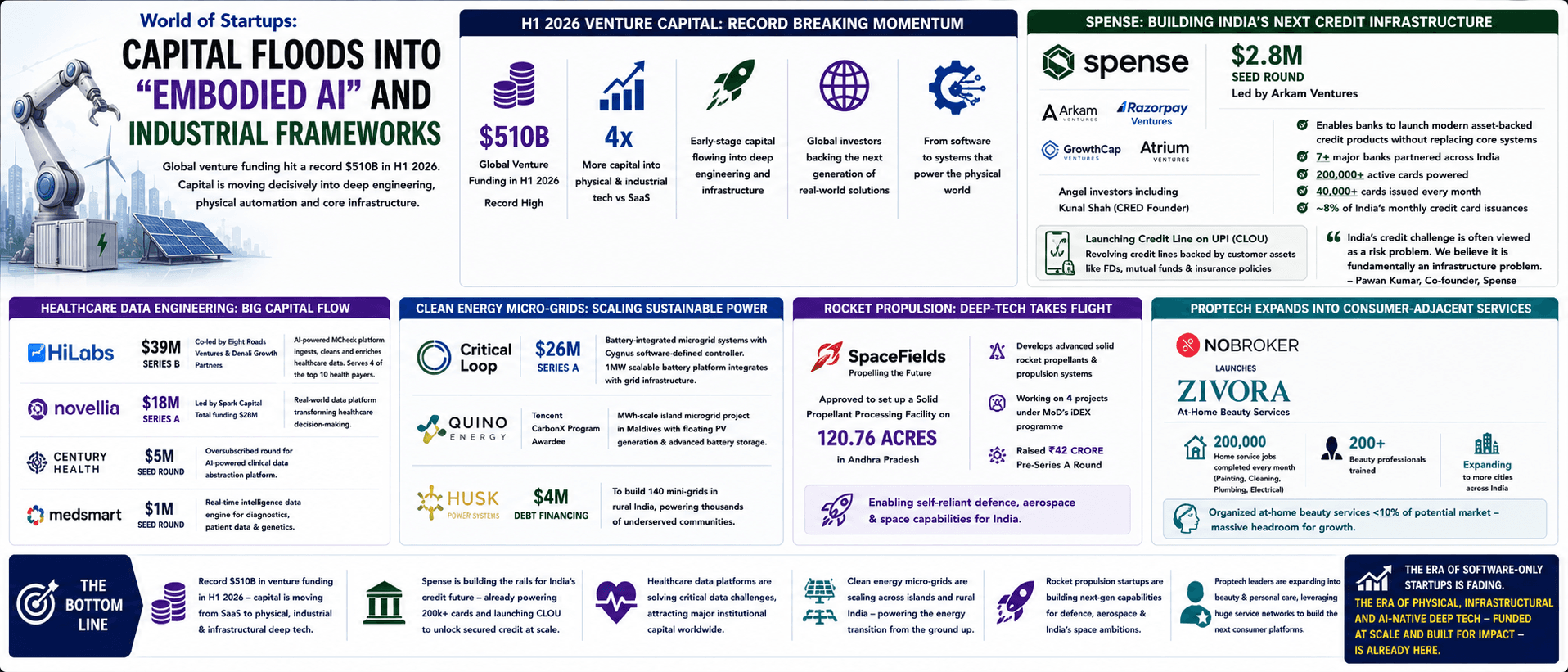

H1 Venture Capital Shatters Records at $510 Billion

V

Author

Vishal Sable

Published

July 8, 2026

Reading Time

3 MIN READ

Spread the Word

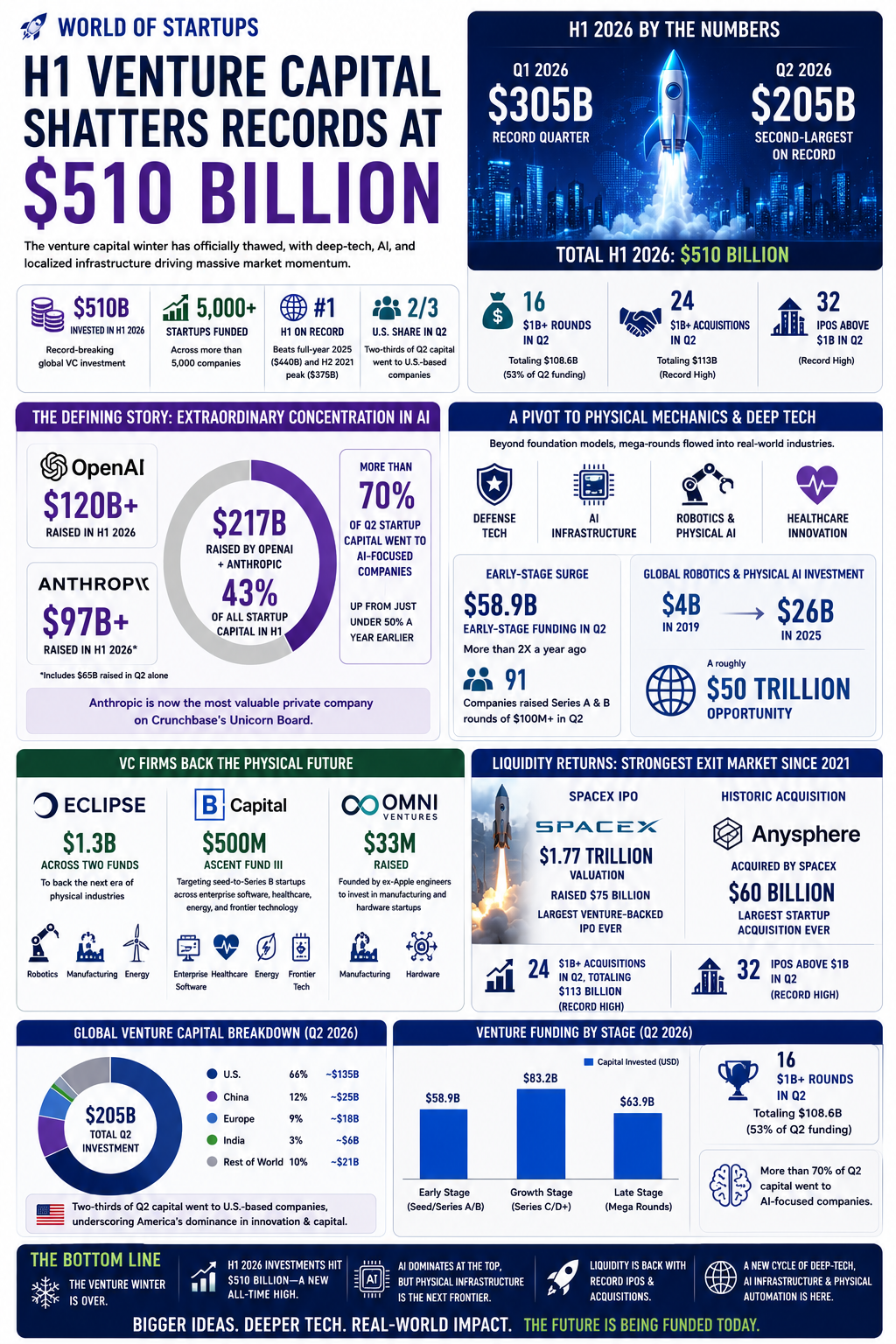

The venture capital winter has officially thawed, with deep-tech, artificial intelligence, and localized infrastructure driving massive market momentum. Global venture investors put a record **$510 billion** into startups in the first half of 2026, according to Crunchbase data published July 2. The single six-month total beats out the $440 billion deployed across the entire year of 2025 and surpasses the previous half-year peak of $375 billion from the second half of 2021. The first quarter alone accounted for a record $305 billion in investments, while the second quarter—the second-largest on record—added another $205 billion across more than 5,000 startups.

The defining characteristic of this funding surge is its extraordinary concentration. OpenAI and Anthropic together commanded **$217 billion—43% of all startup capital in H1**. Anthropic raised $65 billion in Q2 alone—close to a third of global venture funding for the period—and became the most valuable private company on Crunchbase's Unicorn Board. More than 70% of Q2 startup capital went to AI-focused companies, up from just under 50% a year earlier.

While foundation labs pulled in a massive chunk of the cash, early-stage funding saw a significant pivot toward physical mechanics. A total of 16 companies raised billion-dollar rounds in Q2, totaling $108.6 billion—53% of second-quarter funding. Beyond foundation models, large funding rounds were raised by startups working on **defense, AI infrastructure, robotics, and healthcare**. Early-stage funding reached approximately $58.9 billion in Q2—more than double a year ago—with 91 companies raising Series A and B rounds of $100 million or more. Physical AI and robotics attracted significant capital, with venture investment in global robotics and physical AI growing from around $4 billion in 2019 to $26 billion in 2025. Industry experts describe the space—encompassing warehouse robotics, AI-native factories, and energy infrastructure automation—as a roughly **$50 trillion opportunity**.

Venture capital firms are responding to this shift. Eclipse raised $1.3 billion across two funds to back the next era of physical industries, including robotics, manufacturing, and energy. B Capital closed its Ascent Fund III at $500 million targeting seed-to-Series B startups developing technologies across enterprise software, healthcare, energy, and frontier technology. And Omni Ventures, founded by ex-Apple engineers, raised $33 million to invest in manufacturing and hardware startups.

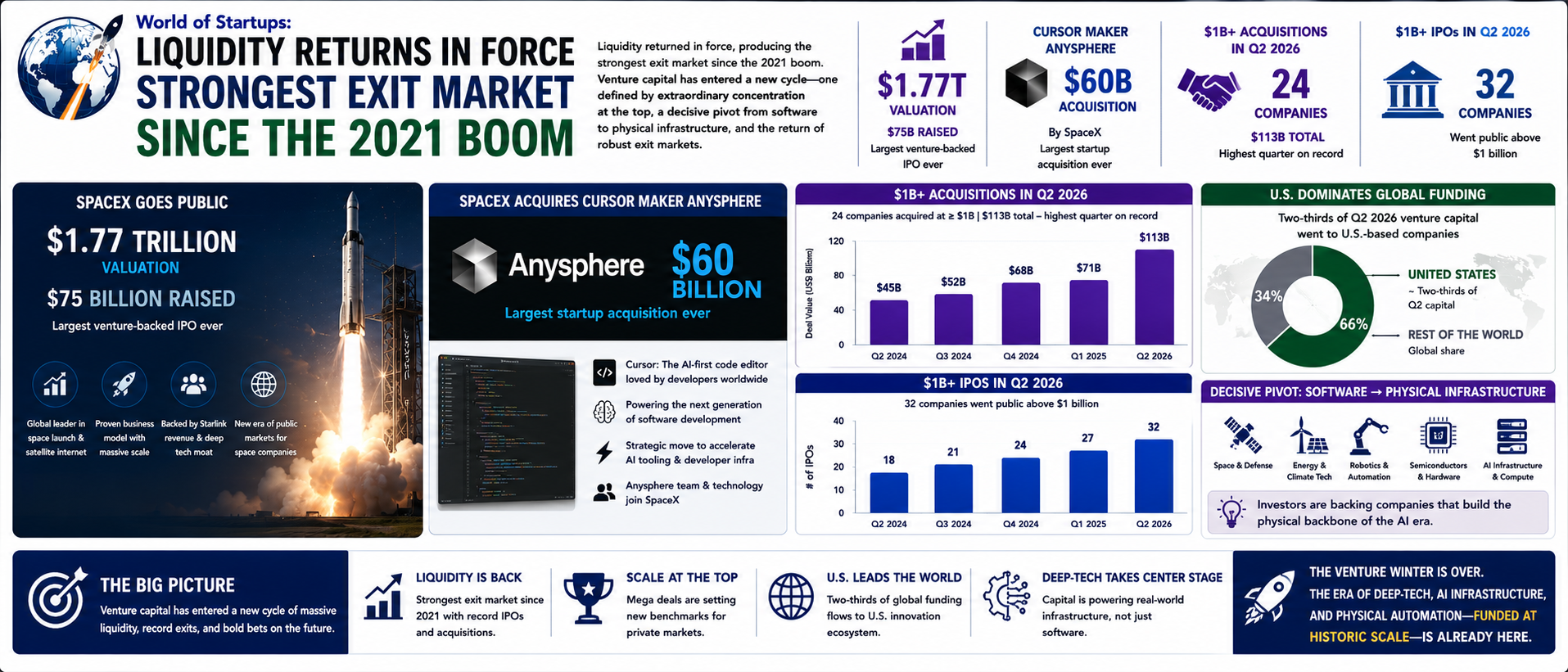

Liquidity returned in force, producing the strongest exit market since the 2021 boom. SpaceX went public at a $1.77 trillion valuation, raising $75 billion in the largest venture-backed IPO ever, then confirmed the acquisition of Cursor maker Anysphere for **$60 billion**—the largest startup acquisition ever. Twenty-four companies were acquired at prices at or above $1 billion in Q2, totaling $113 billion—the highest quarter on record—while 32 companies went public above $1 billion.

The United States again dominated global funding, with two-thirds of Q2 capital going to U.S.-based companies. The data confirms that venture capital has entered a new cycle—one defined by extraordinary concentration at the top, a decisive pivot from software to physical infrastructure, and the return of robust exit markets. The era of the venture winter is over. The era of deep-tech, AI infrastructure, and physical automation—funded at historic scale—is already here.