Back to News

News AlertWorld of Startup’s

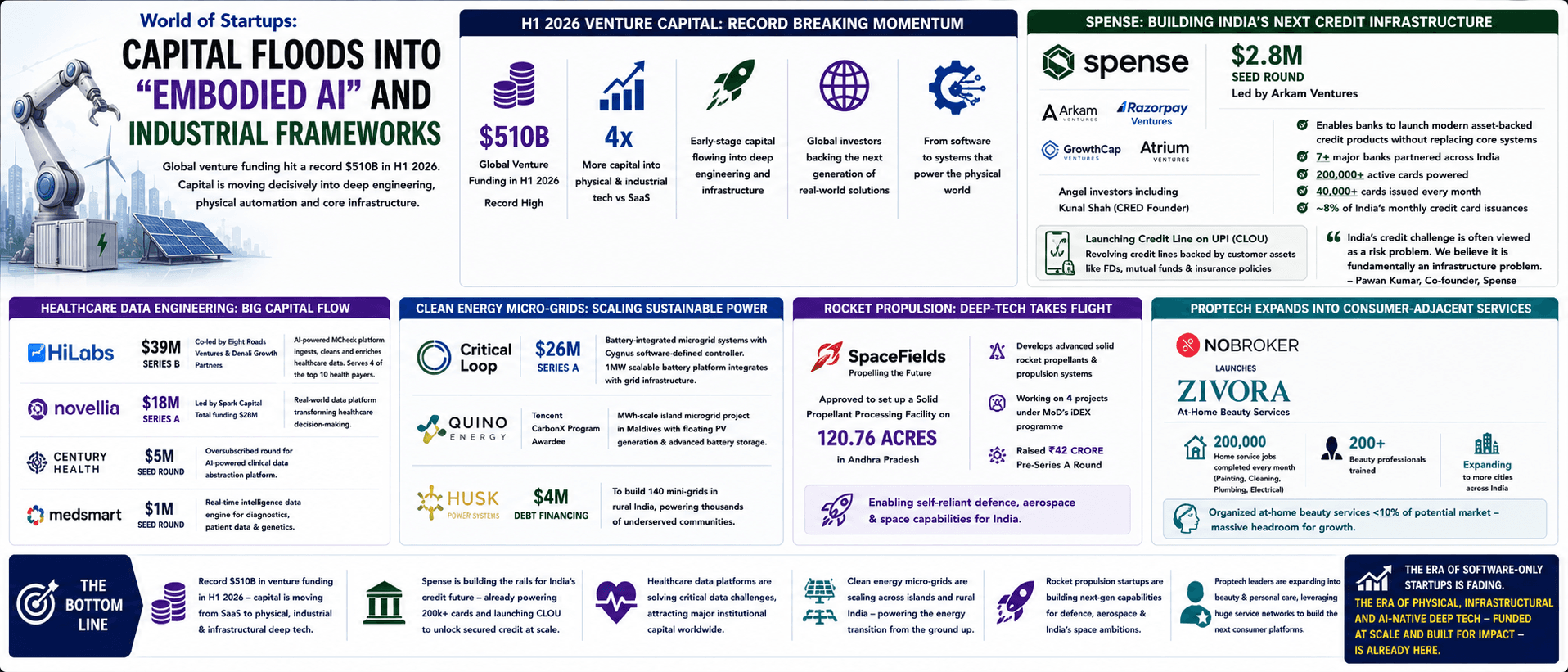

H1 Venture Capital Sweeps to a Historic $510 Billion

V

Author

Vishal Sable

Published

July 2, 2026

Reading Time

6 MIN READ

Spread the Word

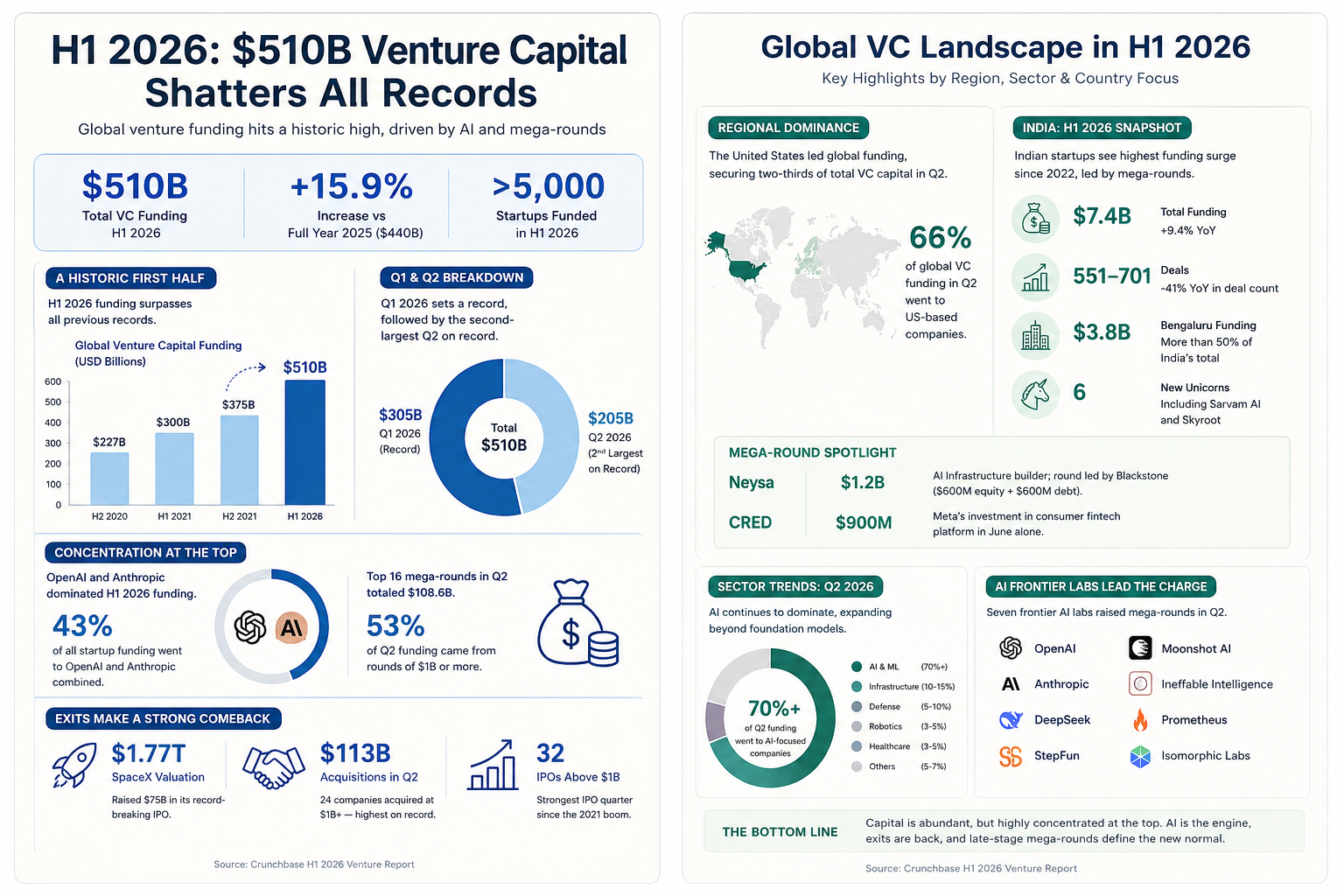

Venture capital is flowing at the fastest rate in history, completely eclipsing prior tech booms, though the funding is heavily concentrated at the absolute top. According to a landmark market intelligence report released today by Crunchbase, global venture capital funding hit a staggering **$510 billion** in the first half of 2026. This single six-month total beats out the capital deployed across the entire year of 2025 ($440 billion), marking the largest first half in venture capital history.

The Latest News

The $510 billion raised in H1 2026 surpassed the previous half-year peak of $375 billion set in the second half of 2021. The first quarter alone accounted for a record $305 billion** in investments, while the second quarter—the second-largest on record—added another **$205 billion across more than 5,000 startups. To the surprise of absolutely no one, artificial intelligence drove the boom.

The defining characteristic of this funding surge is its extraordinary concentration at the top. OpenAI and Anthropic together accounted for $217 billion—43% of all startup funding in the first half**. Anthropic alone raised **$65 billion in the second quarter, close to a third of all global venture funding for the period, making it the most valuable private company on the Crunchbase Unicorn Board. The company surpassed OpenAI on the leaderboard after SpaceX exited via its record-breaking IPO. AI-focused companies took more than 70% of all startup capital in Q2, up from just under 50% a year earlier.

Sixteen companies raised billion-dollar rounds in the second quarter, totaling $108.6 billion—53% of the quarter's funding. Seven of these were frontier labs, including China's DeepSeek, StepFun, and Moonshot AI; the UK's Ineffable Intelligence; and US-based Prometheus and Isomorphic Labs. Beyond foundation models, the boom has spread into AI infrastructure, defense, robotics, and healthcare.

Exits returned in force, producing the strongest liquidity market since the 2021 boom. SpaceX went public at a **$1.77 trillion** valuation, raising $75 billion in the offering, and confirmed a $60 billion acquisition of Anysphere, the maker of the AI coding tool Cursor. Twenty-four companies were acquired at prices at or above $1 billion in Q2, totaling $113 billion—the highest quarter on record—while 32 companies went public above $1 billion.

Regional Dominance

The United States again dominated global funding, with two-thirds of startup capital in Q2 going to US-based companies. The US share was down from 83% in Q1 but in line with proportions from a year earlier.

In regional ecosystems like India, the startup funding pipeline hit $7.4 billion** for H1 2026, marking the highest surge since 2022. The total represents a 9.4% increase from a year earlier, though the number of funding rounds plunged 41%, underscoring a sharp shift in investor preference toward larger, late-stage bets over broad-based capital deployment. Indian startups raised the $7.4 billion across 551–701 deals during the first half. June alone saw a spike with $2 billion raised, mostly driven by AI and fintech, which together grabbed over half the total funding. Bengaluru kept its crown as India's startup capital, attracting **$3.8 billion—more than half of all funding. Six new unicorns joined the club, including Sarvam AI and Skyroot.

This boom was spearheaded by mega-rounds. AI infrastructure builder Neysa secured a massive $1.2 billion** capital raise led by Blackstone, comprising $600 million in primary equity and $600 million in debt financing. And **Meta's landmark $900 million investment into consumer fintech platform CRED in June alone accounted for more than half of the month's funding, highlighting the dominance of late-stage companies in attracting investor capital.

The Bottom Line

July 2026 marks a historic moment for global venture capital. The $510 billion raised in six months has shattered all previous records, fueled almost entirely by the AI boom. Yet the headline number masks a stark reality: two companies—OpenAI and Anthropic—accounted for 43% of all funding. For anyone not building a frontier lab, the useful read is that capital is still available if you can plausibly claim adjacency to compute, defense, robotics, or clinical AI, and that the exit window has reopened for the first time in a while. The rest is a bet on two companies.