Back to News

News AlertWorld of Startup’s

Tech Shakes Up the Primary Market and Wealth Management

V

Author

Vishal Sable

Published

July 4, 2026

Reading Time

9 MIN READ

Spread the Word

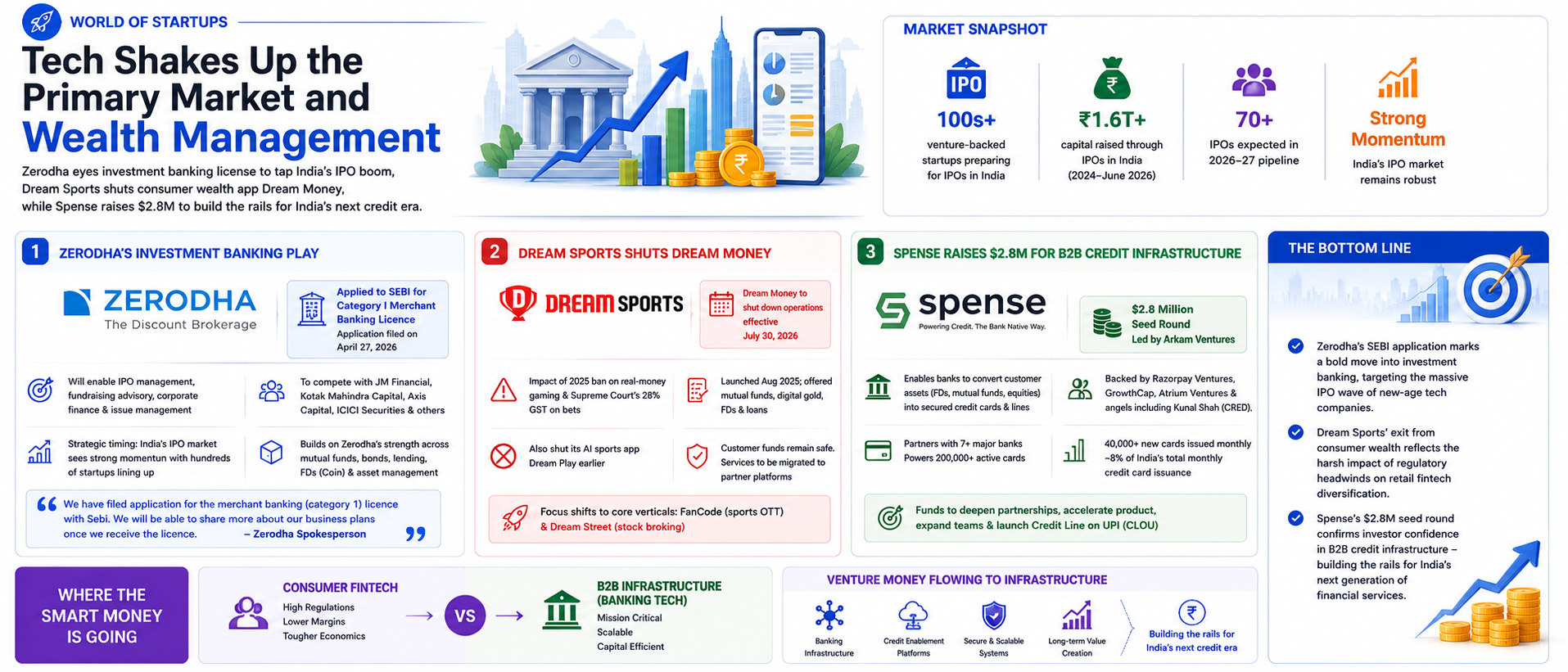

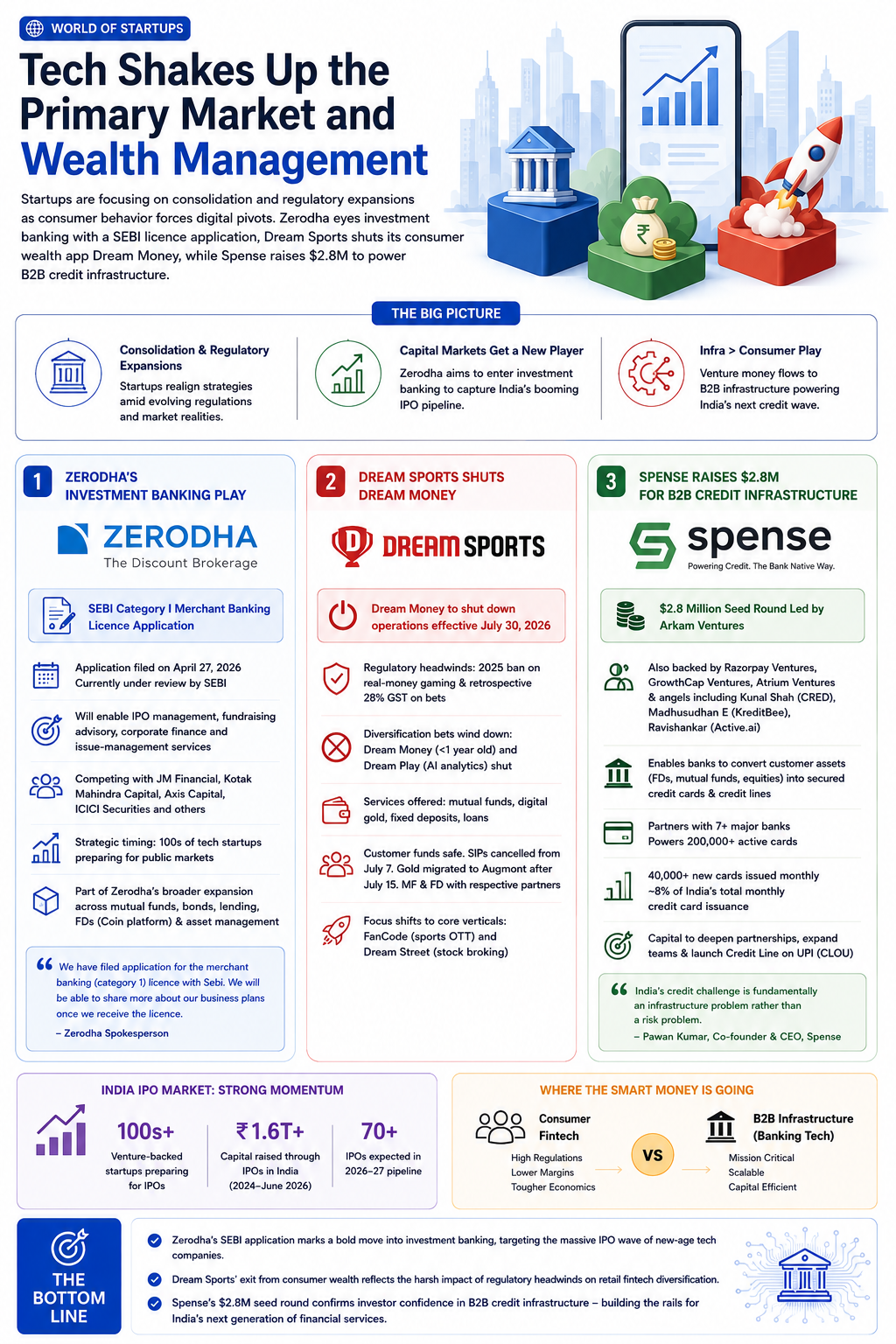

Startups are focusing on consolidation and regulatory expansions as consumer behavior forces digital pivots. Major structural movements are hitting the ecosystem today. Digital broking giant Zerodha has applied for a SEBI license to officially enter investment banking, aiming to capture the massive pipeline of new-age tech startups preparing for public IPOs. Simultaneously, the retail fintech market is consolidating. While gaming-tech major Dream Sports shuttered its consumer wealth app Dream Money, banking infrastructure startup Spense bagged major seed funding backed by Arkam Ventures and CRED founder Kunal Shah, showing that the real venture money is moving to back-end B2B payment systems.

Zerodha’s Investment Banking Play

India’s largest retail broker is preparing to significantly expand its financial services footprint. Zerodha Corporate Advisors Private Limited has applied to the Securities and Exchange Board of India (SEBI) for a Category I merchant banking licence. The application was filed on April 27 and is currently under review by the regulator.

If approved, the licence would allow Zerodha to manage initial public offerings (IPOs), advise companies on fundraising strategies, and provide corporate finance and issue-management services. The move positions Zerodha in direct competition with established investment banking players such as JM Financial, Kotak Mahindra Capital, Axis Capital, and ICICI Securities, which currently dominate the space.

Confirming the development, a Zerodha spokesperson stated: “We have filed application for the merchant banking (category 1) licence with Sebi. We will be able to share more about our business plans once we receive the licence”.

The timing is strategic. India’s IPO market is seeing strong momentum, with hundreds of venture-backed startups and new-age technology firms preparing to tap public markets over the next few years. Zerodha’s entry could intensify competition for public market mandates, particularly among technology-led and digitally native companies. The development follows Zerodha’s recent efforts to broaden its consumer financial products ecosystem, including the launch of fixed deposit investments on its Coin platform and its existing presence across mutual funds, bonds, lending, and asset management.

Dream Sports Shuts Dream Money

In a sharp contrast to Zerodha’s expansion, Dream Sports—the parent entity behind fantasy gaming giant Dream11—has announced the shutdown of its fintech arm, Dream Money, less than a year after its August 2025 launch. The platform will discontinue all business operations effective July 30, 2026.

The closure comes amid sweeping regulatory changes impacting India’s real-money gaming industry. Following the government’s 2025 ban on all forms of real-money gaming, including fantasy sports, and the Supreme Court’s upholding of a retrospective 28% GST levy on bets placed through such platforms, several gaming firms have either shut down, downsized, or diversified their businesses. Dream Sports had launched Dream Money as part of its diversification strategy, offering mutual funds, digital gold, fixed deposits, and loans to leverage its massive user base. However, the platform’s closure—along with the earlier shuttering of its AI-powered sports analytics app, Dream Play—signals a strategic retreat from newer ventures.

The company has assured customers that their funds and investments remain safe. Active SIPs will be cancelled from July 7, 2026. Digital gold holdings will be migrated to partner platform Augmont after July 15. Mutual fund investors can manage their portfolios directly with the respective asset management companies, while fixed deposits will continue to be serviced by partner banks. Dream Sports will now channel resources toward its more established verticals, including sports OTT platform FanCode and stock broking service Dream Street.

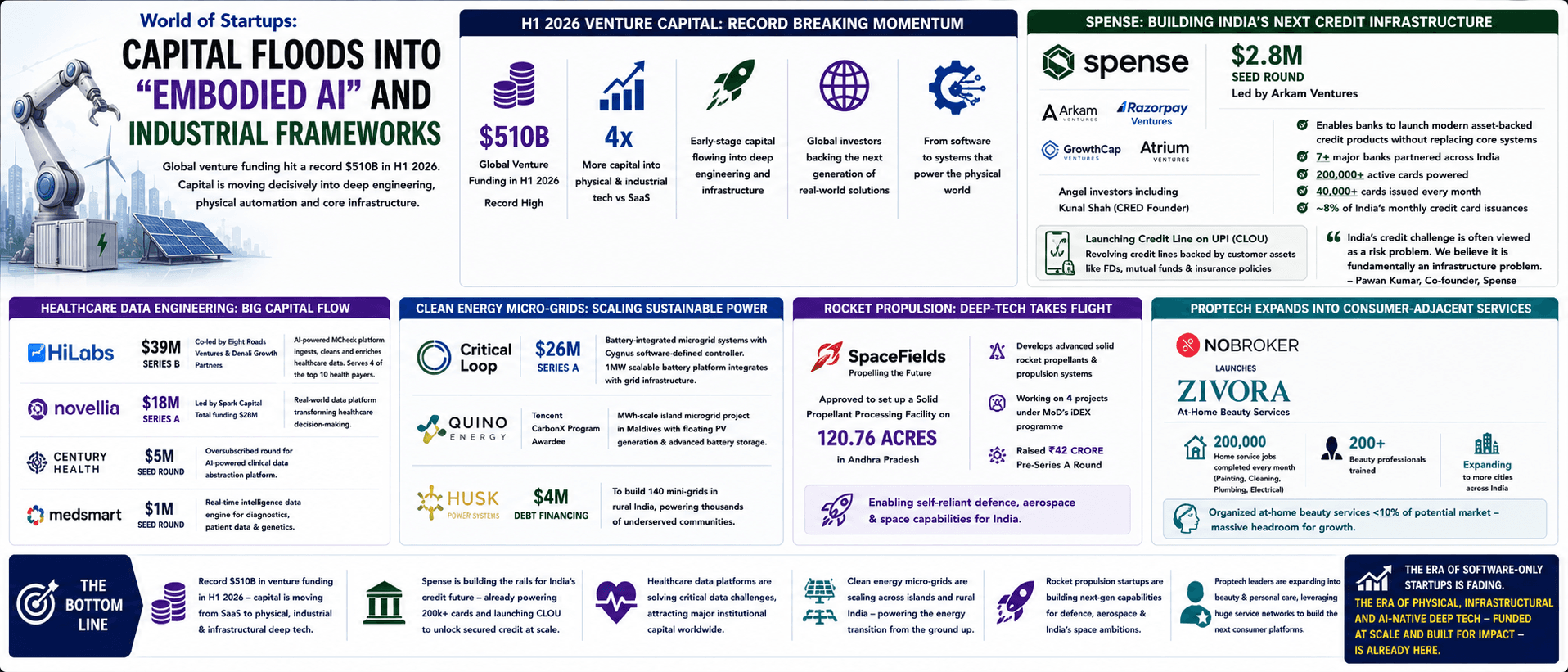

Spense Raises $2.8 Million for B2B Credit Infrastructure

While consumer-facing fintech struggles, venture money is flowing into B2B infrastructure. Bengaluru-based banking infrastructure startup Spense has raised $2.8 million in a seed funding round led by Arkam Ventures. The round also saw participation from Razorpay Ventures, GrowthCap Ventures, Atrium Ventures, and angel investors including CRED founder Kunal Shah, Madhusudhan E (KreditBee), and Ravishankar (Active.ai).

Spense provides a bank-native infrastructure layer that integrates with existing systems, enabling institutions to launch modern credit products without replacing their technology. The company enables banks to convert customer assets—such as fixed deposits, mutual funds, and equities—into secured credit cards and credit lines efficiently and at scale. Spense already partners with seven major banks, including one of the country’s largest public sector banks, and powers over 200,000 active cards, with more than 40,000 new cards issued monthly—accounting for nearly 8% of India’s total monthly credit card issuance.

The fresh capital will deepen partnerships with financial institutions, accelerate product development, and expand engineering and go-to-market teams. A key priority is the launch of Credit Line on UPI (CLOU). Pawan Kumar, Co-founder and CEO of Spense, framed the company’s mission: “India’s credit challenge is fundamentally an infrastructure problem rather than a risk problem”. Bala Srinivasa of Arkam Ventures added that Spense is building “foundational infrastructure for India’s next credit era”.

The Bottom Line

July 2026 marks a clear divergence in India’s startup ecosystem. Zerodha’s SEBI application signals a push into institutional capital markets, aiming to capture the IPO pipeline of new-age tech companies. Dream Sports’ shutdown of Dream Money reflects the harsh reality of regulatory headwinds for consumer fintech diversification. And Spense’s $2.8 million seed round, backed by Arkam Ventures and Kunal Shah, confirms that the smart money is moving to B2B infrastructure—building the rails for India’s next generation of credit rather than chasing retail users. The era of consumer fintech expansion is giving way to an era of infrastructure-first, B2B-focused financial technology.