Back to News

News AlertWorld Money

The Great Efficiency Pivot

V

Author

Vishal Sable

Published

June 29, 2026

Reading Time

16 MIN READ

Spread the Word

Fintech in mid-2026 is no longer about burning cash to capture market share. It is about profitability, infrastructure, and the quiet automation of financial logic. Three announcements this month capture this transformation perfectly. The Boston Consulting Group's Global FinTech Report 2026 reveals a sector that has not just recovered but matured, with global revenues surpassing half a trillion dollars and profitability becoming the new benchmark. Real-world asset tokenization has crossed a $30 billion milestone, proving that institutional finance is finally embracing blockchain infrastructure. And three of Japan's largest banks have signed a historic memorandum to jointly issue a yen stablecoin, signalling a regional shift toward unified digital settlement systems. Meanwhile, at the daily use level, Lloyds Bank and Stripe have partnered to give small businesses instant access to enterprise-grade payment tools through mobile tap-to-pay. Together, these developments tell a single story: fintech is entering its efficiency era.

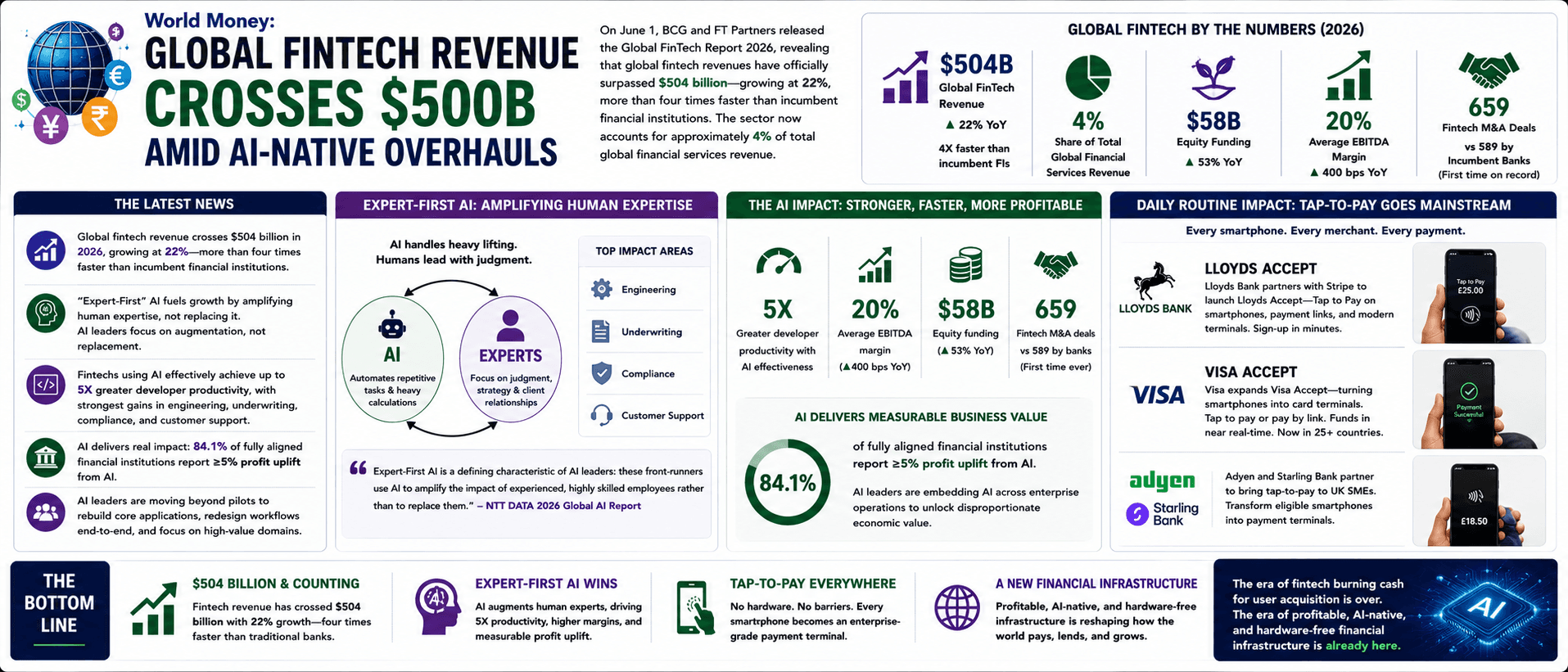

The BCG Global Fintech Report 2026: $504 Billion and Climbing

The headline from Boston Consulting Group and FT Partners' Global FinTech Report 2026 is unambiguous: the sector is in full resurgence. Global fintech revenues reached a record $504 billion in 2025, growing more than four times faster than traditional financial services. But the more important story is not the size of the rebound. It is what is driving it: real profitability, selective investment, and a fundamental shift in how financial services are built and delivered. The report identifies fintech's current moment as materially different from both the boom years and the correction period. The sector has rebounded into a more mature, more selective, and more strategically consequential landscape—one where the basis of competition is shifting from digital nativity and category creation to profitable scale, regulatory readiness, and the translation of new technologies into durable operating advantage. Among the 85 largest public fintechs, average EBITDA margins reached 20% in 2025, up four percentage points in a single year. This is not a sector scraping by on growth promises; it is a sector earning its place. Equity funding jumped 53% to $58 billion, while fintech companies out-acquired banks in M&A for the first time on record. Late-stage funding (Series E and beyond) grew over 210% from 2023 to 2025, while seed-stage funding contracted by 10%. Capital is concentrating around companies with proven economics, not early-stage bets. The fintech spring, as the report puts it, is in full bloom—but it rewards execution, not just ambition. Regionally, Asia-Pacific led growth at 25%, driven by digital banking and crypto platforms in Japan, South Korea, Singapore, and Indonesia. Europe grew 24%, supported by neobanks expanding into adjacent products. North America grew 21%, broadly in line with the global average. But the single biggest untapped opportunity in the entire report is B2B financial services. Fintechs have barely scratched the surface of business lending, insurance, and deposits. Workflows like accounts payable, expense management, and reconciliation are still largely manual. The platforms that crack this will define the next decade of fintech growth.

The Rise of Agentic Commerce: When AI Agents Do the Financial Thinking

Among the seven trends shaping the next five years of financial services, the BCG report highlights one above all: the emergence of agentic commerce. This is the development of highly specialised AI agents that execute legal financial logic, travel fare calculations, and automated risk scoring autonomously. The scale is already visible. BCG estimates that a first wave of agentic commerce could represent roughly **$375 billion of US e-commerce spending in the short term**, with $1 trillion eventually becoming agent-assisted out of a $1.9 trillion addressable base. According to other industry forecasts, AI agents could influence over 50% of online spend by 2030, with the agentic commerce market growing from $130 billion in 2025 to $1.7 trillion by 2030. Scaled agentic commerce will take longer to emerge and will likely start in low-ticket, repeatable categories such as household supplies and groceries, where error costs are low and value is clear. But the direction is unmistakable. The report identifies AI adoption, operational transformation, and the rise of agentic commerce as key trends shaping the future of the industry. As one industry observer noted, "AI systems increasingly assist with product discovery, purchasing decisions and transaction execution". Traditional financial rails, however, were not built for the speed of software, creating a significant infrastructure gap. Chargebacks911, a global leader in dispute resolution, warns that these innovations introduce new layers of complexity for merchants attempting to understand transaction behavior, manage risk, and resolve disputes effectively. As transactions become more sophisticated, merchants need a clearer understanding of what is happening throughout the customer journey. The challenge is not a lack of data but a lack of visibility. This is precisely where AI-driven compliance and risk platforms are stepping in—not just to automate, but to illuminate.

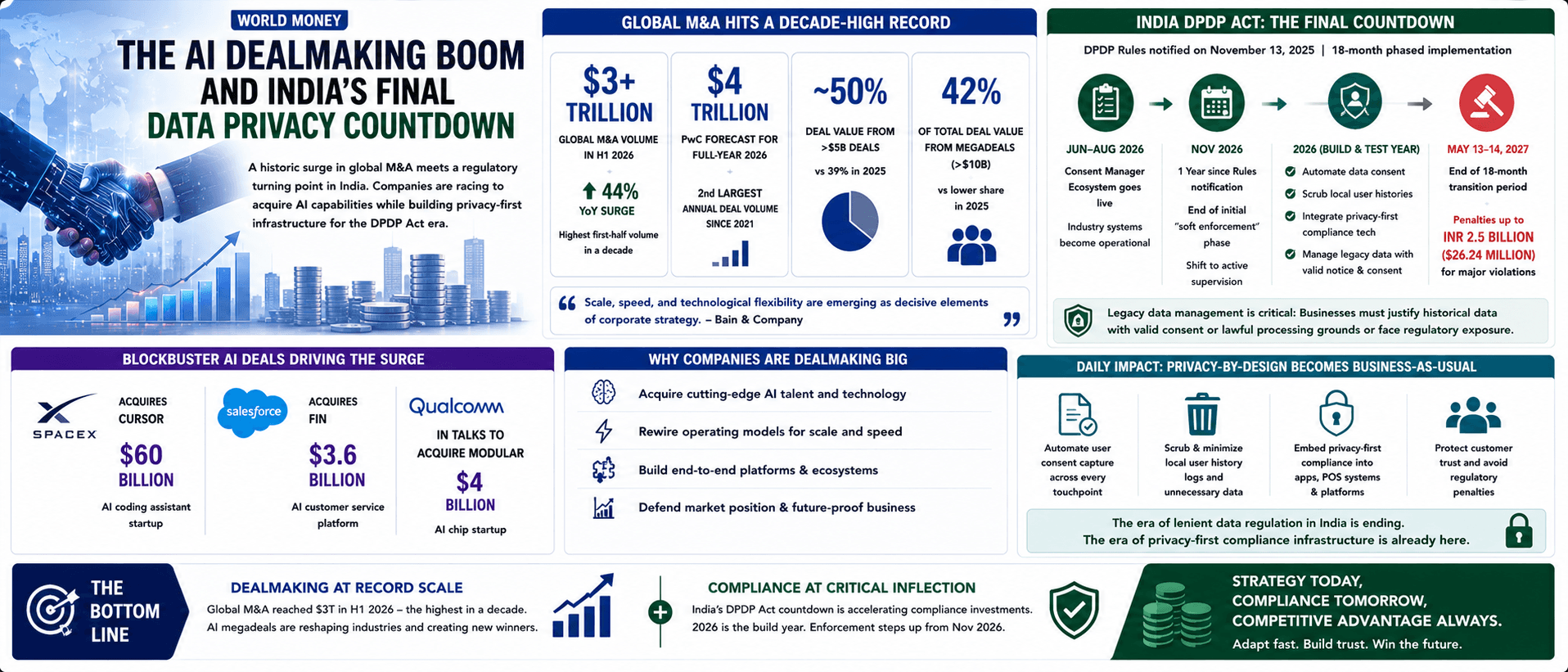

Tokenization & Regional Stablecoins: The $30 Billion Bridge

The second major trend reshaping fintech infrastructure is the tokenization of real-world assets. The on-chain RWA market grew from roughly $5.5 billion in early 2025 to around **$30 billion by mid-2026**, led by tokenized US Treasuries near $12.9 billion and private credit around $19 billion. This momentum is coming from traditional finance, not retail traders, with BlackRock, JPMorgan, Franklin Templeton, and others building tokenized funds and settlement systems. The promise is fractional ownership, 24/7 settlement, and programmability. But the risks are real: the token is only as strong as the legal structure, the custodian, and the regulatory wrapper behind it. Securitize CEO Carlos Domingo recently projected that tokenized equities could drive the RWA market from its current $30 billion size to **$5 trillion**. With stocks and ETFs serving as the primary catalyst rather than Treasury instruments, the growth trajectory is accelerating. In parallel, regional stablecoin infrastructure is taking shape. On June 10, 2026, Japan's three largest banks—MUFG, SMBC, and Mizuho—signed a memorandum of understanding to jointly issue a yen-based stablecoin and begin live commercial transactions during fiscal year 2026, which ends March 31, 2027. The token will be issued through a trust agreement, with the three banks acting as joint settlors and a trust bank or similar institution serving as trustee. The banks have established a voluntary council to design the issuance infrastructure, system design, governance, and operating processes. They have named corporate settlement, cross-border payments, and digital commerce as target use cases. The plan grew out of a demonstration experiment selected in November 2025 under the Financial Services Agency's FinTech proof-of-concept hub, which tested using the stablecoin to settle purchases of stocks, bonds, and investment funds. This is a significant departure from the fragmented stablecoin landscape. Yen-based stablecoins currently account for less than $50 million of the market, with JPYC the largest at about $18 million. A coin backed by MUFG, SMBC, and Mizuho would be far larger than existing yen tokens. The move aligns with Japan's broader push to integrate digital assets into its financial system, including new rules that open access to the national payment infrastructure for foreign trust-type stablecoins.

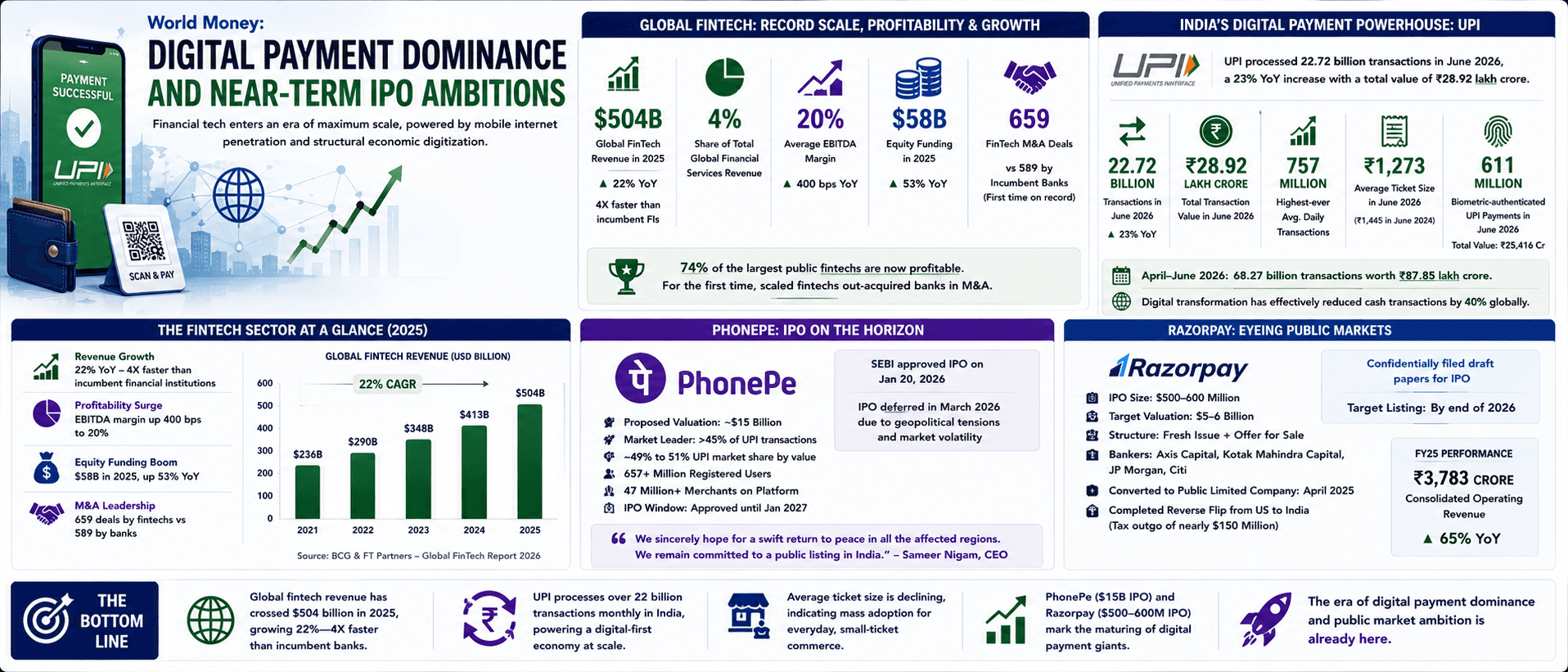

Daily Use: Lloyds Accept Brings Enterprise Payments to Every High Street

While infrastructure deals grab headlines, the most tangible impact of fintech's efficiency era is visible at the daily use level. On June 9, 2026, Lloyds Bank and Stripe launched Lloyds Accept, a new suite of payment tools for UK small businesses. The proposition gives small businesses access to the same payments infrastructure as the world's leading payments teams at companies like Amazon or OpenAI. Powered by Stripe Connect, Lloyds Accept is integrated directly into the Lloyds Business Account. Sign-up times are typically within minutes. The tools include Tap to Pay on smartphones, payment links, and modern terminal devices for in-person transactions. Lloyds Accept supports Tap to Pay on iPhone or Tap to Pay on Android, enabling businesses to accept contactless payments wherever they trade—from on-site customer locations and markets to community and school events—using only a smartphone and the Lloyds Accept app. At checkout, customers simply hold their card or digital wallet near the merchant's device to pay securely. Amanda Murphy, CEO of Lloyds Business & Commercial Banking, framed the offering in practical terms: "Simple, flexible payment solutions are essential for growth. These new tools enable customers to get set up and start trading instantly—supporting healthy cash flow, which is critical for every stage of growth". Eileen O'Mara, Chief Revenue Officer at Stripe, added: "A small business on any UK high street can now run on the same payments infrastructure as the largest and fastest-growing companies in the world. World-class financial tools shouldn't be gated by size". Lloyds serves over 26 million individual customers and more than one million business customers. The partnership brings Stripe's global payments technology to a massive UK small-business base, democratising access to modern payment infrastructure. For small businesses, this means instant access to enterprise-grade tools without the heavy hardware setups that have historically been a barrier to entry.

Conclusion: The Efficiency Era Has Arrived

Taken together, these three narratives reveal a coherent picture of fintech's trajectory in mid-2026. The BCG report confirms that the sector has matured into a profitable, selective, and strategically consequential industry. Agentic commerce is moving from experiment to expectation, with AI agents set to influence over half of online spend by 2030. RWA tokenization has crossed a $30 billion milestone, with institutions betting on blockchain infrastructure to unlock fractional ownership and 24/7 settlement. Japan's mega-banks are uniting behind a single stablecoin framework, signalling regional convergence in digital settlement systems. And Lloyds Accept is bringing enterprise-grade payments to every UK high street. The through-line is clear. In 2024, fintech was about disruption. In 2025, it was about consolidation. In 2026, it is about efficiency, infrastructure, and profitable scale. The companies and countries that succeed will be those that can automate financial logic, tokenize real-world assets, and democratise access to world-class payment infrastructure—all while maintaining profitability and regulatory discipline. The fintech spring is in full bloom. But it rewards execution, not just ambition.