Back to News

News AlertWorld Money

UK’s FCA Lowers Capital Requirements for Stablecoin Issuers

V

Author

Vishal Sable

Published

July 4, 2026

Reading Time

9 MIN READ

Spread the Word

As digital asset frameworks mature globally, regulators are shifting from outright crackdowns to creating clear, business-friendly guardrails. The past week has delivered two major developments confirming this trajectory: the UK's Financial Conduct Authority finalizing its crypto rulebook with a significantly lower capital requirement for stablecoin issuers, and Worldline, Crédit Agricole, and Mastercard successfully executing France's first live AI-agent retail payment.

The Latest News

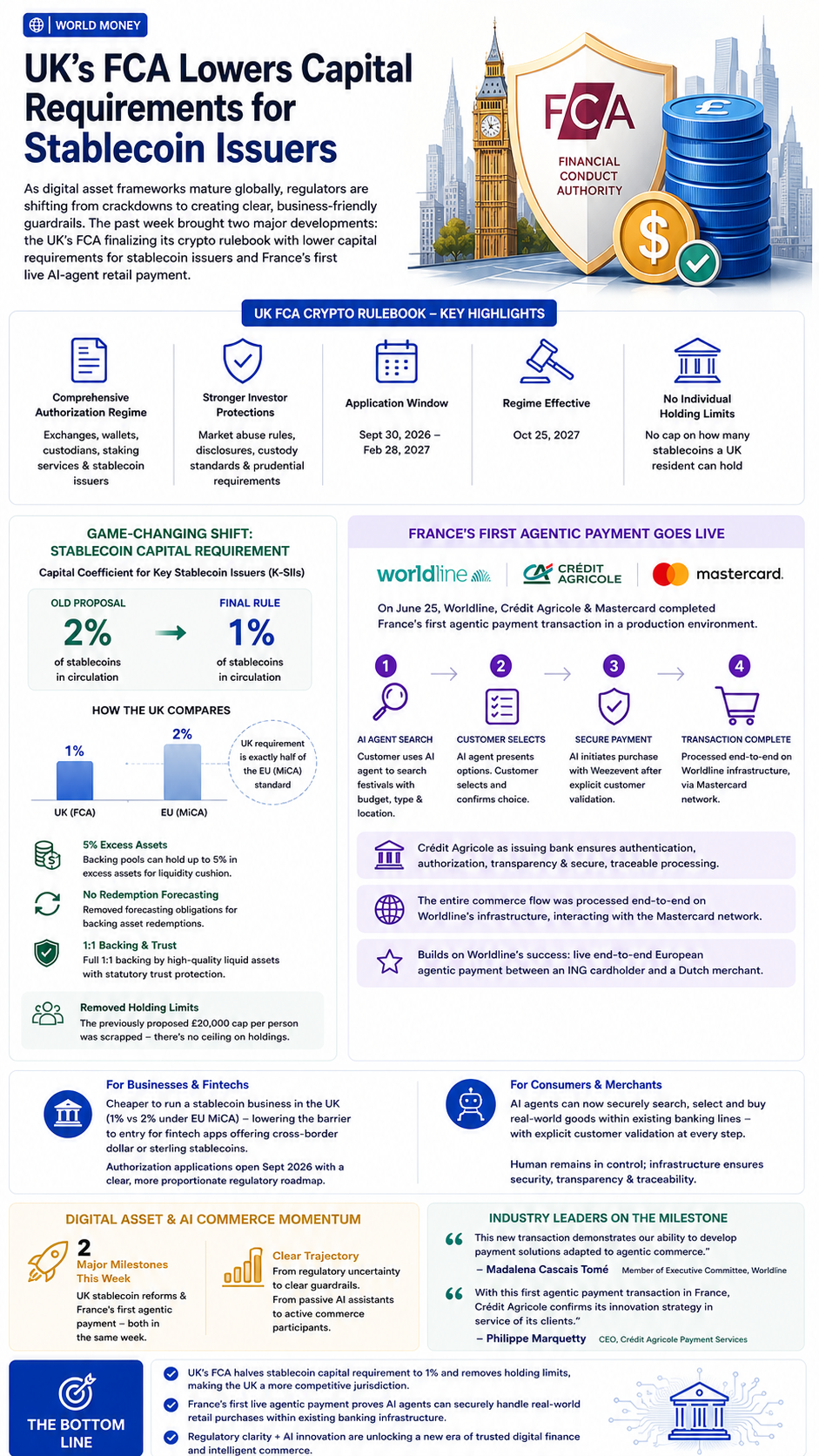

On June 30, the UK's Financial Conduct Authority (FCA) published its final policy statements, finalizing a broad crypto rulebook that brings exchanges, wallets, custodians, staking services, and qualifying stablecoin issuers into a full authorization regime. The framework introduces mandatory licensing, custody standards, market-abuse protections, disclosure rules, and prudential requirements. Crypto firms will be able to apply for authorization between September 30, 2026, and February 28, 2027, ahead of the mandatory regime taking effect on October 25, 2027.

The biggest change, however, is the stablecoin capital requirement. The FCA reduced the proposed capital coefficient for Key Stablecoin Issuers (K-SIIs) from 2% to 1% of the value of stablecoins in circulation. This direct halving of the capital buffer follows extensive industry feedback that the earlier threshold was too costly for firms trying to compete with offshore, U.S., and EU issuers.

The reduction puts the UK's requirements at exactly half of what the EU demands under its Markets in Crypto-Assets (MiCA) regulation, which requires a 2% capital coefficient. The FCA's payment and digital finance executive director, David Gill, acknowledged that the originally proposed standard was too high, and that significant industry feedback confirmed the compliance cost pressure was excessive.

Beyond the capital coefficient reduction, the FCA also removed redemption forecasting obligations for backing assets—meaning stablecoin issuers no longer need to predict and report how many tokens they expect customers to redeem at any given time. Backing pools can now hold up to 5% in excess assets, giving issuers room to maintain a small liquidity cushion without regulatory friction. The framework still requires full 1:1 backing by high-quality liquid assets, along with statutory trust arrangements to protect customer funds.

Perhaps the most notable change that didn't make the headline was the abandonment of individual holding limits. The Bank of England had previously floated a £20,000 cap on how much any single person could hold in regulated stablecoins—a proposal that was reversed during 2025 consultations, meaning there's now no ceiling on how many stablecoins a UK resident can hold. The removal of holding limits is particularly relevant for institutional players, as a £20,000 cap would have been a non-starter for any serious trading desk or treasury operation.

France's First Agentic Payment Goes Live

Simultaneously, on June 25, Worldline, Crédit Agricole, and Mastercard announced they had successfully completed France's first agentic payment transaction in a production environment. The milestone demonstrates that autonomous AI agents can securely initiate and complete payments on behalf of users, moving beyond simple digital assistants into active commerce participants.

The use case centered on a Crédit Agricole customer using an AI agent to search for festivals. By setting specific parameters—budget, event type, and location—the customer received a range of options from the AI agent. The customer then selected and confirmed their choice, instructing the AI to initiate the purchase process with event solutions provider Weezevent. Critically, the transaction was only executed after explicit customer validation, with Crédit Agricole as the issuing bank maintaining a central role in authentication and authorization. Specific identifiers ensured transparency of the agentic transaction and guaranteed secure, traceable processing across the entire payment chain. The entire commerce flow was processed end-to-end on Worldline's infrastructure, interacting with the Mastercard network.

Madalena Cascais Tomé, member of Worldline's Executive Committee, stated: "This new transaction, carried out in France with Crédit Agricole, demonstrates our ability to develop payment solutions adapted to agentic commerce. At Worldline, through our platforms and expertise, we connect and orchestrate the entire ecosystem—merchants, banks, payment networks—to guarantee interoperable transactions compliant with market standards". Philippe Marquetty, CEO of Crédit Agricole Payment Services, added: "With this first agentic payment transaction in France, Crédit Agricole confirms its innovation strategy in service of its clients. As a bank, we play a key role in guaranteeing secure, traceable, and fully controlled journeys, adapted to future purchasing experiences".

The initiative builds on Worldline's success in facilitating a live end-to-end European agentic payment between an ING cardholder and a Dutch merchant, unveiled at Money20/20 earlier this year. Together, these projects demonstrate that agentic commerce is moving from theoretical roadmaps to live production environments across multiple European markets.

Daily Routine Impact

The FCA's lower capital requirement makes it significantly cheaper to run a stablecoin business in the UK, substantially lowering the barrier to entry for fintech apps offering cross-border dollar or sterling stablecoins. With authorization applications opening in September 2026, firms now have a clear roadmap to operate within a regulated framework that is more proportionate than the EU's MiCA regime.

Meanwhile, France's first agentic payment transaction proves that autonomous digital assistants can now securely authenticate and purchase real-world goods within standard banking lines. The explicit customer validation requirement ensures that humans remain in control, while the underlying infrastructure demonstrates that agentic commerce can function within existing banking and merchant environments while respecting market security and traceability requirements.

The Bottom Line

July 2026 marks a pivotal moment for digital asset regulation and AI-driven commerce. The UK's FCA has positioned the country as a more competitive jurisdiction for stablecoin issuance, with capital requirements half those of the EU and no individual holding limits. Meanwhile, France's first agentic payment transaction proves that AI agents can securely handle real-world retail purchases within existing banking infrastructure. The era of regulatory uncertainty is giving way to an era of clear, business-friendly guardrails—and the era of AI agents as passive assistants is giving way to an era of AI agents as active commerce participants.